THE IRS SHADOW: LEGAL DEFENSES AGAINST UNREPORTED NIL INCOME AND AGENT FRAUD

The seismic shift in the landscape of amateur athletics, precipitated by the National Collegiate Athletic Association (NCAA) adoption of the Interim Name, Image, and Likeness (NIL) Policy on July 1, 2021, has fundamentally transitioned the student-athlete from a recipient of educational aid to a commercial enterprise and federal taxpayer. This evolution has created a profound intersection between sports law, intellectual property, and federal tax jurisprudence, exposing athletes, content creators, and professional influencers to a sophisticated array of tax liability traps and predatory representation. As these individuals navigate the complexities of high-stakes endorsements, the "IRS Shadow" looms large, manifesting in the form of rigorous reporting requirements, the doctrine of constructive receipt, and the persistent threat of agent fraud.

The tax system’s treatment of NIL income is uncompromising, viewing it not as a "scholarship-adjacent" stipend but as entrepreneurial business income subject to the same strictures as any other for-profit venture. For the athlete-taxpayer, financial sovereignty is contingent upon transforming a reactive fear of audits into a proactive legal shield, leveraging specific statutory defenses and Internal Revenue Service (IRS) guidance to insulate brand equity from the devastating consequences of unreported income and fraudulent concealment by intermediaries.

THE TAX ANATOMY OF NIL INCOME: STATUTORY FRAMEWORKS AND REPORTING THRESHOLDS

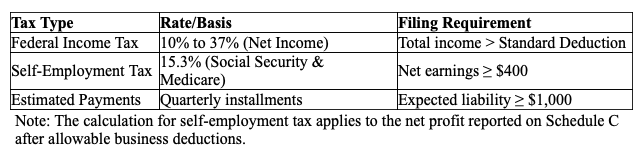

The foundational principle of the federal tax system, as articulated in Internal Revenue Code (IRC) Section 61, defines gross income as "all income from whatever source derived," specifically including compensation for services, fees, and commissions. In the NIL context, this definition captures a diverse array of revenue streams, from social media influencer content and brand endorsements to autograph fees, promotional appearances, and merchandise sales. The IRS has clarified that NIL income is typically classified as self-employment income rather than wages, unless an employer-employee relationship is established under the common law "control" test.

CLASSIFICATION AS SELF-EMPLOYMENT INCOME

When an athlete operates as an independent contractor, they are engaged in a trade or business for tax purposes. This classification triggers a dual tax burden: federal income tax at progressive rates ranging from 10% to 37%, and a self-employment tax of 15.3%, which covers Social Security and Medicare obligations. The self-employment tax is calculated on 92.35% of the athlete's net earnings, provided those earnings exceed the $400 filing threshold.

THE EVOLUTION OF INFORMATION REPORTING THRESHOLDS

The mechanisms used by the IRS to track NIL income have undergone significant regulatory adjustments through 2024, 2025, and 2026. Third-Party Settlement Organizations (TPSOs) and payment platforms are central to this tracking. While the transition has been marked by shifting floors, the 2026 tax season introduces permanent changes under the One Big Beautiful Bill Act (OBBBA).

The reduction of the 1099-K threshold to $600 in 2026 ensures that even micro-influencers and collegiate athletes with modest endorsements are captured within the IRS’s automated data-matching systems. Furthermore, any NIL deal valued at $600 or more must be vetted and reported to the College Sports Commission (CSC) via the NIL Go platform to ensure the transaction has a legitimate business purpose and does not constitute "pay-to-play".

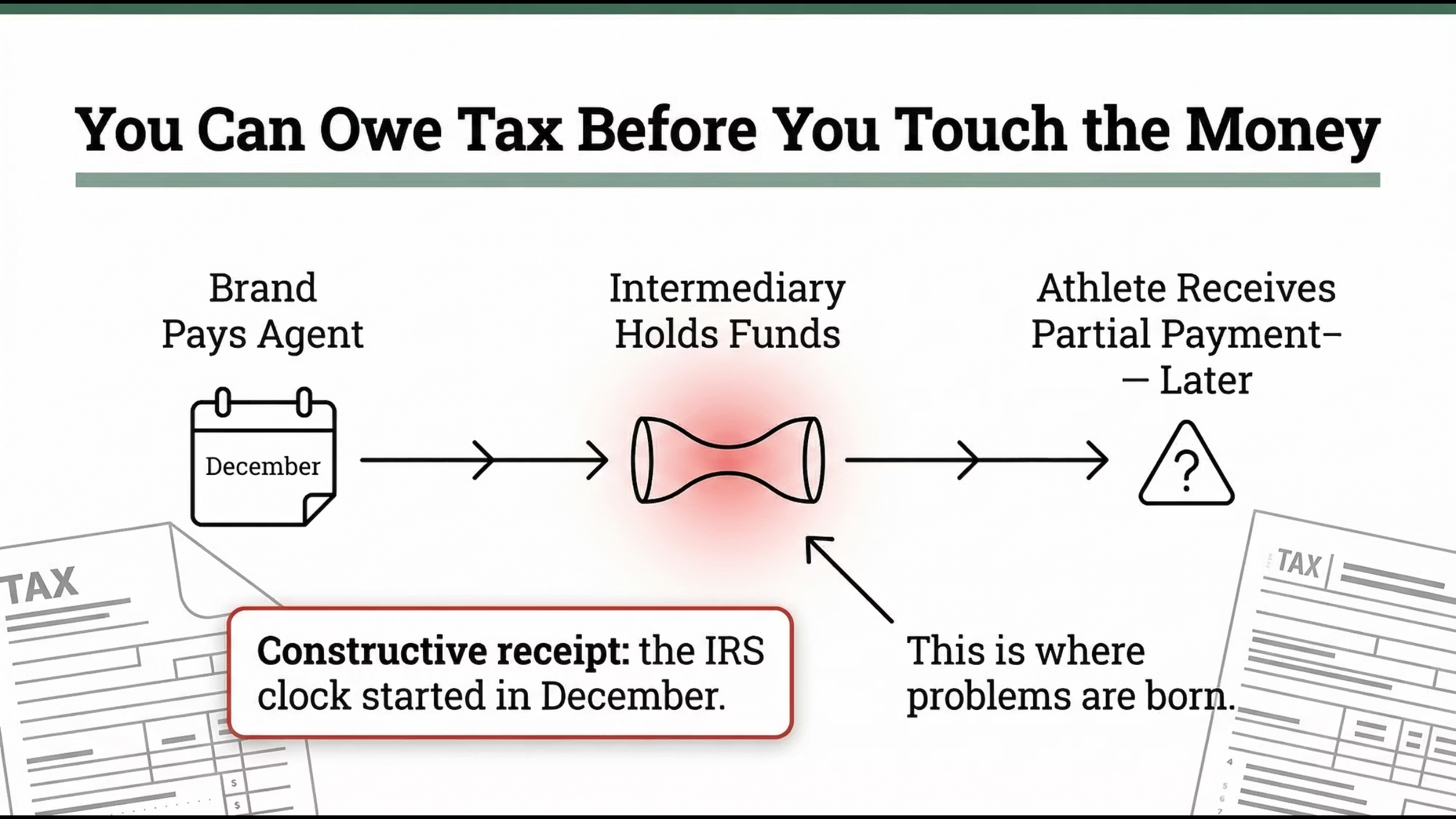

CONSTRUCTIVE RECEIPT: THE INVISIBLE LIABILITY TRAP

One of the most dangerous misconceptions in the NIL ecosystem is the belief that tax liability is deferred until income is physically deposited into the athlete's personal bank account. The IRS doctrine of "constructive receipt" dictates that income is taxable in the year it is made available to the taxpayer without substantial limitation or restriction, regardless of whether it is in their physical possession.

THE AGENT-PRINCIPAL NEXUS

For athletes, the doctrine of constructive receipt has profound implications when dealing with agents, managers, or NIL collectives. IRS Publication 525 explicitly states that "income received by an agent for you is income you constructively received in the year the agent received it". If an agent secures a $50,000 endorsement deal and the brand pays the agency directly in December, the athlete is liable for the taxes on that $50,000 for that tax year, even if the agent does not remit the funds to the athlete until January of the following year.

This principle extends to third-party agreements. If an athlete contractually directs a sponsor to pay a portion of their earnings to a creditor or a family member, the athlete must still include that amount in their gross income at the time the third party receives it. This "assignment of income" does not shift the tax burden; the athlete remains the primary taxpayer for the full gross amount of the contract.

BARTER AND NON-CASH COMPENSATION

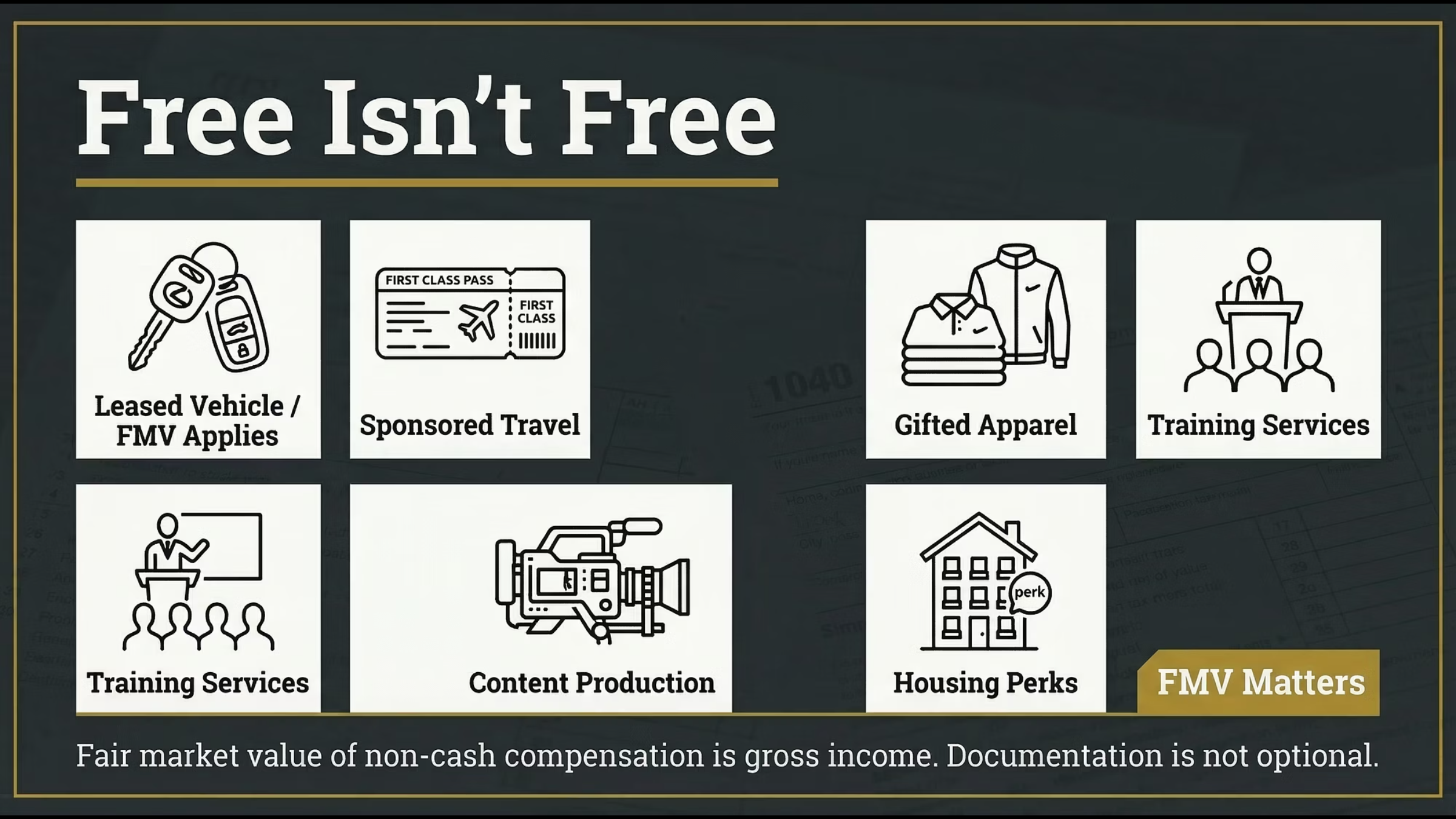

The IRS has signaled that it is increasingly focused on non-cash NIL compensation, which is frequently overlooked by young athletes. These benefits, which include free apparel, luxury vehicle leases, complimentary travel, and high-performance training services, are taxable at their fair market value (FMV).

The valuation of these items creates significant audit risk. For example, if an athlete receives a luxury vehicle for promotional use, they must report the FMV of the lease as income on Schedule C. Conversely, they may be entitled to deduct the portion of the vehicle's use that is strictly for business purposes (e.g., traveling to appearances), but they must maintain rigorous mileage logs to substantiate the deduction. Failure to report non-cash perks triggers not only back taxes but also accuracy-related penalties based on the FMV of the omitted items.

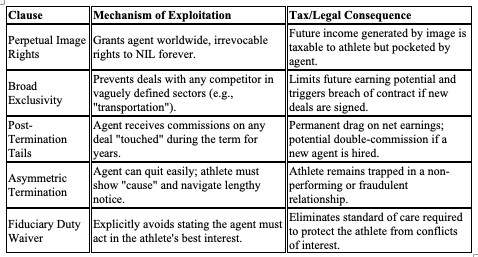

DISMANTLING PREDATORY AGENT TACTICS AND CONTRACTUAL FRAUD

The rapid deregulation of collegiate athletics has allowed for the proliferation of unregulated agents who may utilize predatory contract terms to exploit the gap between an athlete's market value and their tax sophistication. These intermediaries often use the complexity of tax law to conceal earnings or shift financial risks onto the athlete.

CONTRACTUAL RED FLAGS AND LEGAL HAZARDS

Attorneys must scrutinize representation agreements for "poison pill" clauses that can lead to long-term financial devastation. Predatory agents frequently include provisions that extend their reach far beyond the actual services provided.

Contractual Red Flags & Legal Hazards © 2026 Ball 'N Play™ Sports Agency PLLC

One of the most egregious tactics involves the concealment of gross earnings. Agents may negotiate a deal for a gross amount but only report a "net" figure to the athlete, pocketing the difference while leaving the athlete liable for the tax on the full gross amount under the constructive receipt rule. This is often facilitated by "hidden fees" for content production or travel that are quietly deducted from the athlete's pay without proper documentation, making them nondeductible for the athlete but still part of their taxable gross income.

THE FIDUCIARY DEFENSE

A critical legal defense against agent overreach is the assertion of fiduciary duty. In most jurisdictions, an agent acts as a fiduciary to their client, requiring them to act with the utmost good faith, disclose all conflicts of interest, and prioritize the client's financial health. Agreements that lack explicit fiduciary language or attempt to waive these duties should be viewed as prima facie evidence of predatory intent. For the athlete, ensuring that the agent is contractually bound to fiduciary standards provides a legal basis for challenging hidden commissions and unauthorized deductions in court.

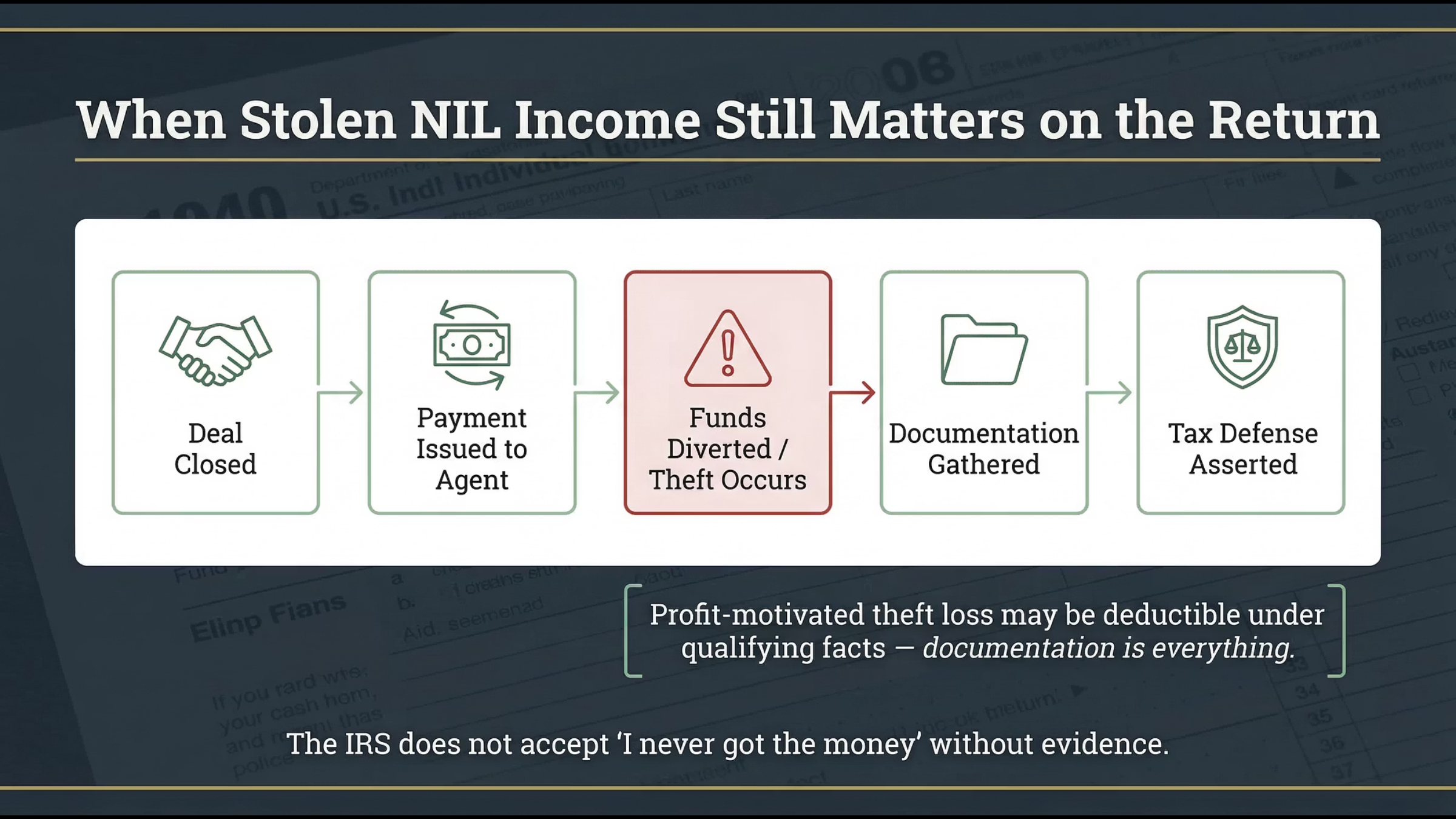

STATUTORY DEFENSES: THE SECTION 165 THEFT LOSS REBIRTH

When an athlete falls victim to agent fraud or investment scams—such as the "pig butchering" schemes identified by the IRS—they face a double hardship: the loss of the principal funds and a tax bill on the income that was stolen. Historically, the Tax Cuts and Jobs Act (TCJA) of 2017 severely restricted theft loss deductions, limiting them to losses incurred in federally declared disasters for the tax years 2018 through 2025.

THE MARCH 2025 IRS CHIEF COUNSEL MEMORANDUM

A transformative development occurred in March 2025 when the IRS Office of Chief Counsel issued Memorandum (CCM) 202511015. This guidance clarified that while personal theft losses remain restricted, losses incurred in a "transaction entered into for profit" under IRC Section 165(c)(2) are still deductible.

For an athlete, the relationship with an agent is inherently a transaction entered into for profit. Therefore, if an agent misappropriates NIL funds, the athlete can leverage Section 165(c)(2) to claim a theft loss deduction, effectively offsetting the income that was constructively received but never enjoyed.

The CCM establishes three strict criteria that must be satisfied to claim this defense:

Illegal Taking: The loss must result from an act that constitutes criminal theft under the laws of the state where it occurred, and it must have been done with criminal intent.

Profit Motive: The taxpayer must demonstrate that their primary intention in the transaction was to achieve an economic advantage.

No Prospect of Recovery: The loss is only deductible in the year it is discovered, and only to the extent that there is no "reasonable prospect of recovery" through insurance, litigation, or other claims.

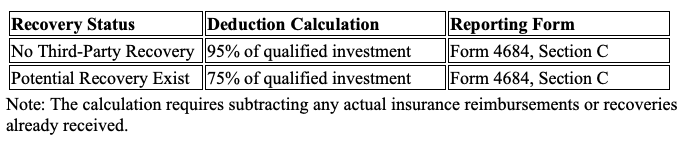

CALCULATING THE THEFT LOSS DEDUCTION

The deductible amount is generally limited to the taxpayer's "adjusted basis" in the stolen property—which, in the case of NIL income, is the amount of income that has been reported or is reportable to the IRS.

The CCM distinguishes these profit-motivated losses from "personal casualty losses" such as romance scams or kidnapping ransoms, which remain nondeductible under the OBBBA unless tied to a declared disaster. For the athlete, the "profit motive" of an NIL deal serves as the gateway to this critical tax relief.

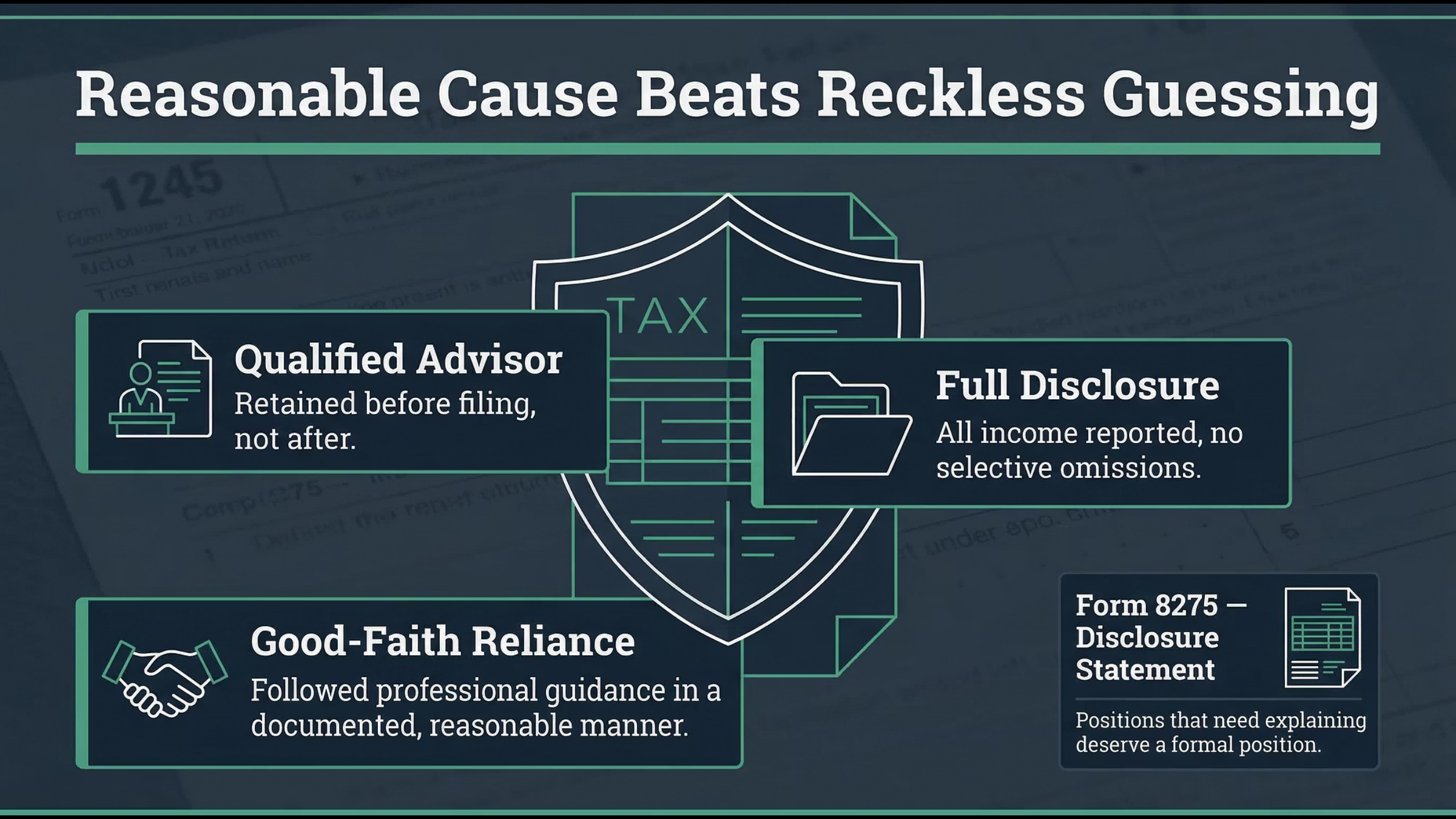

INSULATING AGAINST PENALTIES: THE REASONABLE CAUSE DEFENSE

Even in cases where an athlete fails to report NIL income accurately, they can avoid accuracy-related penalties by establishing "reasonable cause" and showing that they acted in "good faith". The IRS imposes a 20% penalty on underpayments attributable to negligence or a substantial understatement of income tax.

THE NEONATOLOGY TEST FOR PROFESSIONAL RELIANCE

The most potent defense against these penalties is the athlete's reliance on a qualified tax professional. Under the Tax Court’s decision in Neonatology Associates, P.A. v. Commissioner, a taxpayer can avoid penalties if they satisfy a three-prong burden of proof :

Competence of the Advisor: The athlete must have hired a professional (e.g., CPA, tax attorney) with sufficient expertise in the specific tax matter, such as NIL income or multi-state athlete sourcing.

Full Disclosure of Information: The athlete must have provided the advisor with all necessary and accurate information to evaluate the tax treatment. This includes disclosing all 1099s, barter deals, and agent-withheld amounts.

Good-Faith Reliance: The athlete must have actually followed the advisor’s judgment in good faith.

For collegiate athletes, the IRS and courts often consider the taxpayer’s "experience, knowledge, education, and sophistication" in determiningwhether reliance was reasonable. An 18-year-old athlete with no prior business experience who relies on an agency-provided accountant has a stronger reasonable cause defense than a veteran professional athlete with a sophisticated family office.

THE ROLE OF FORM 8275: DISCLOSURE AS A SHIELD

To proactively insulate the brand from penalties, tax attorneys can utilize Form 8275 (Disclosure Statement) or Form 8275-R (Regulation Disclosure Statement). By filing these forms with the tax return, the athlete "adequately discloses" items or positions that are not otherwise obvious on the return. This disclosure acts as a safe harbor; even if the IRS eventually disagrees with the tax treatment of an NIL deal, the disclosure typically prevents the imposition of the 20% accuracy-related penalty, provided the position had a "reasonable basis".

MULTI-STATE HAZARDS: THE JOCK TAX AND DIGITAL NEXUS

The "jock tax" is not a separate levy but a specific application of nonresident income sourcing rules that treats out-of-state athletes as temporary employees of the state where they perform services. For the modern athlete, the jock tax applies to any income earned while physically present in a state, including NIL appearances, signing events, and content shoots.

THE DUTY-DAY FORMULA MECHANICS

States typically use a "duty-day" formula to calculate the portion of an athlete's total compensation subject to their state income tax. A duty day is defined as any day spent in a state for professional obligations, including practices, media junkets, and promotional activities.

$$\text{Sourced Income} = \text{Total NIL Compensation} \times \left( \frac{\text{Duty Days in State}}{\text{Total Duty Days per Year}} \right)$$

As state tax agencies become more aggressive, they are counting not just game days, but every moment of professional obligation. For example, if an athlete spends ten days in California for a Nike content shoot and their total work year is 200 days, 5% of their entire annual endorsement income may be subject to California's top tax bracket, which can exceed 13%.

THE NEXUS OF CONTENT CREATION

Independent content creators and influencers face a unique sourcing challenge. If an athlete creates and uploads social media content while traveling for an away game or a vacation, that activity can technically create "nexus" in the state where the content was filmed. While many states have de minimis thresholds, some require a nonresident return for a single day of work. Failure to track these locations leads to a risk of double taxation, as the athlete’s home state may not provide a credit for taxes paid to another state if the income was sourced incorrectly under that state's specific laws.

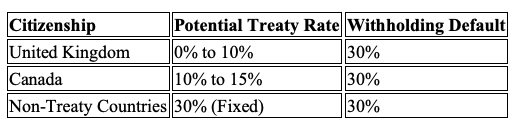

THE INTERNATIONAL ATHLETE DILEMMA: VISAS AND 30% WITHHOLDING

For international student-athletes competing on F-1 visas, NIL income introduces a layer of immigration and tax complexity that can jeopardize their status in the United States. F-1 visas generally prohibit off-campus employment, and while some "passive" NIL income (such as licensing fees) may be permitted, "active" content creation or appearances often violate visa terms.

NONRESIDENT ALIEN (NRA) TAX COMPLIANCE

International athletes are classified as "nonresident aliens" for U.S. tax purposes. This classification subjects their NIL income to a flat 30% withholding tax, which must be withheld at the source by the payor, unless a bilateral tax treaty between the U.S. and the athlete's home country provides a reduced rate.

Many brands and NIL collectives are unaware of these withholding requirements, leading them to pay the international athlete the full amount of the contract. This leaves the athlete with a significant, un-withheld tax liability and places the payor at risk for failing to withhold. For the international athlete, seeking a specialized tax professional is not just about financial optimization; it is a requirement for maintaining legal residency.

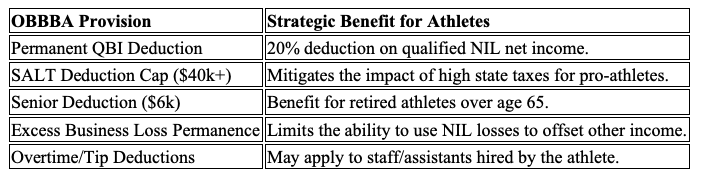

ONE BIG BEAUTIFUL BILL ACT (OBBBA): THE 2026 REGULATORY LANDSCAPE

The One Big Beautiful Bill Act (OBBBA), signed in 2025 and fully implemented for the 2026 tax season, introduced several provisions that impact the athlete-taxpayer’s bottom line.

PERMANENT QBI AND SALT ENHANCEMENTS

The OBBBA made the 20% Qualified Business Income (QBI) deduction permanent for active trades and businesses. This allows athletes operatingas sole proprietors or through pass-through entities (LLCs, S-Corps) to deduct 20% of their net NIL profit from their taxable income, effectively reducing their tax burden.

The act also provides clarity on the permanent nondeductibility of certain expenses, such as investment management fees and unreimbursed employee business expenses. For athletes who function as "small business owners," the OBBBA increases the Section 179 deduction limit to $2.5 million, allowing for the immediate expensing of equipment (e.g., training gear, content creation hardware) purchased for the business.

THE 2026 "DIRTY DOZEN" AND SOCIAL MEDIA AUDITS

The IRS has signaled that it is using modern tools to enforce compliance in the creator economy. "Misleading tax advice on social media" is item #4 on the 2026 Dirty Dozen list, specifically targeting "tax hacks" that suggest NIL income is not taxable if kept in digital wallets or offshore accounts. Furthermore, the IRS reported over 600 social media impersonators in fiscal year 2025, warning that scammers are targeting high-profile individuals by pretending to be IRS agents to obtain sensitive financial data for identity theft.

FORENSIC RECORDKEEPING: BUILDING THE "ORDINARY AND NECESSARY" SHIELD

The ultimate defense against an IRS audit is substantiation. Under IRC Section 162, business expenses must be "ordinary and necessary" for the trade or business to be deductible. For an athlete-entrepreneur, the definition of what is ordinary and necessary is expansive but requires rigorous documentation.

DEDUCTIBLE EXPENSE CATEGORIES FOR NIL ATHLETES

Athletes can significantly reduce their taxable income by accurately tracking business expenses on Schedule C.

Professional Services: Agent commissions, legal fees for contract review, and accounting fees for tax preparation.

Marketing and Branding: Website hosting, social media advertising, and fees for graphic designers or photographers.

Travel and Lodging: Airfare and hotels for promotional tours, signings, or media appearances.

Training and Performance: Payments to specialized coaches or trainers used to maintain the athlete’s brand value (athletic performance).

Home Office: A pro-rata share of rent and utilities if a dedicated space is used exclusively for brand management or content creation.

THE VOLUNTARY DISCLOSURE PRACTICE (VDP) AS A LAST RESORT

For athletes who realize they have unreported NIL income from prior years—often due to a predatory agent failing to disclose earnings—the IRS Voluntary Disclosure Practice (VDP) provides a path to come into compliance without criminal prosecution.

The VDP requires the taxpayer to submit Form 14457 to IRS Criminal Investigation for preclearance. A disclosure is only considered "voluntary" if it occurs before the IRS has received a tip from a third party or initiated an exam. For the athlete, a VDP filing marks a willingness to cooperate, pay the back taxes, interest, and a structured penalty in exchange for closure on the omitted income.

FINANCIAL SOVEREIGNTY: A STRATEGIC SYNTHESIS

The transition of college and professional athletes into the role of federal taxpayers represents a coming-of-age for the industry, but it also creates a landscape fraught with regulatory and predatory peril. The "IRS Shadow" is not an insurmountable threat; rather, it is a management challenge that requires a shift from reactive financial behavior to a proactive legal strategy.

By leveraging the March 2025 CCM to claim theft losses against fraudulent agents, asserting the Neonatology reasonable cause defense to mitigate penalties, and rigorously applying the duty-day formula to multi-state income, the modern athlete can build a career-saving shield. Financial sovereignty in the NIL era is not achieved through the signing of the next contract, but through the vigilant protection of the income that contract generates. Compliance is not merely a bureaucratic requirement; it is a foundational element of brand protection, ensuring that the athlete’s market value is preserved for their future and not sacrificed to an IRS audit or a predatory intermediary. The strategy prioritizing transparency and substantiation transforms complex regulatory hurdles into a competitive edge, allowing the athlete to focus on their performance while their legal defenses secure their legacy.